Managing your finances is not just about saving money or paying bills on time. It is about building a stable and secure future while reducing financial stress in your daily life. Many people believe financial management is only for wealthy individuals or finance experts, but the truth is that anyone can learn how to handle money wisely.

Good financial habits can help you avoid debt, prepare for emergencies, and achieve your long-term goals. Whether you want to buy a home, travel more, start a business, or simply live comfortably, managing your finances properly is one of the most important skills you can develop.

The good news is that financial management does not need to be complicated. With a few smart strategies and consistent habits, you can take control of your money like a professional.

Understand Where Your Money Goes

The first step toward better financial management is understanding your current financial situation. Many people spend money without tracking where it goes, which often leads to unnecessary expenses and financial pressure.

Start by reviewing your monthly income and expenses. Write down every source of income and list all your spending categories, including rent, groceries, transportation, subscriptions, entertainment, and savings.

You may be surprised to discover how much money is spent on small daily purchases. Coffee, online shopping, food delivery, and unused subscriptions can quietly drain your budget over time.

Tracking your spending helps you identify wasteful habits and gives you a clear picture of your financial behavior. Once you know where your money is going, you can make smarter decisions about how to use it.

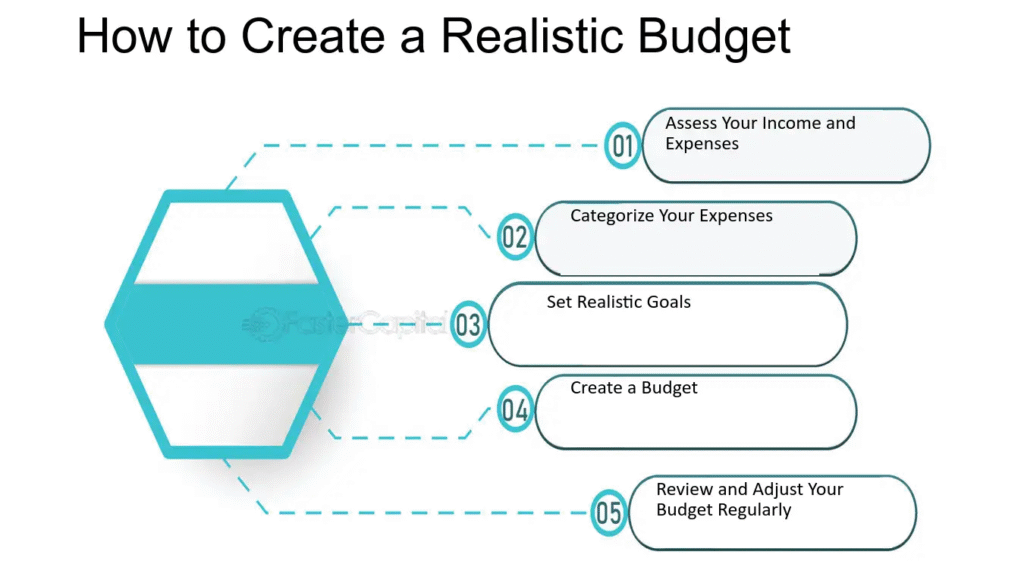

Create a Realistic Budget

A budget is one of the most powerful financial tools available. It helps you control spending, save money, and stay focused on your goals.

The key to successful budgeting is creating a plan that works for your lifestyle. A budget should not feel restrictive or impossible to follow. Instead, it should help you spend with purpose.

One popular budgeting method is the 50/30/20 rule:

- 50% for needs such as housing, groceries, and bills

- 30% for wants like entertainment and dining out

- 20% for savings and debt payments

This method is simple and flexible, making it easier for beginners to manage money effectively.

Review your budget regularly and adjust it when necessary. Life changes, and your financial plan should evolve with it.

Build an Emergency Fund

Unexpected expenses are a part of life. Medical bills, car repairs, job loss, or family emergencies can happen at any time. Without savings, these situations can quickly create financial stress.

An emergency fund acts as a financial safety net. It protects you from relying on credit cards or loans during difficult times.

Start small if necessary. Even saving a little each month can make a difference over time. Aim to build enough savings to cover at least three to six months of living expenses.

Keep this money in a separate savings account so you are less tempted to spend it on non-emergencies.

Having emergency savings provides peace of mind and financial confidence.

Avoid Unnecessary Debt

Debt can become one of the biggest obstacles to financial stability. While some types of debt, such as mortgages or education loans, may be necessary, high-interest consumer debt can quickly become overwhelming.

Credit cards are especially dangerous when balances are not paid in full each month. Interest charges can grow rapidly and make it difficult to escape debt cycles.

Before making a purchase, ask yourself whether it is truly necessary. Avoid buying things simply because they are on sale or because others are spending money on them.

If you already have debt, focus on paying it down strategically. Many people use either the debt snowball method or the debt avalanche method.

The debt snowball method focuses on paying off smaller debts first for motivation, while the avalanche method prioritizes debts with the highest interest rates to save money over time.

Both methods can be effective when combined with discipline and consistency.

Learn to Save Consistently

Saving money is not about how much you earn. It is about developing consistent habits.

Many people wait until the end of the month to save whatever is left over, but often there is nothing remaining. A better strategy is to treat savings like a regular monthly expense.

Set up automatic transfers to your savings account every time you receive income. This approach makes saving easier and removes the temptation to spend first.

Having clear savings goals can also increase motivation. You may want to save for a vacation, a new car, retirement, or a home down payment.

When your goals are specific, saving becomes more meaningful and easier to maintain.

Invest for Long-Term Growth

Saving money is important, but investing allows your money to grow over time. Inflation gradually reduces the value of cash, which means money sitting in a regular savings account may lose purchasing power in the future.

Investing helps build long-term wealth and financial security.

Beginners often feel intimidated by investing, but it does not need to be complicated. Many simple investment options are designed for people with little experience.

Index funds, mutual funds, retirement accounts, and exchange-traded funds are common investment choices for long-term growth.

The most important factor in investing is consistency and patience. Successful investing is usually about steady growth over many years rather than trying to get rich quickly.

Avoid making emotional investment decisions based on fear or excitement. Markets naturally rise and fall over time, and long-term discipline often produces the best results.

Improve Your Financial Knowledge

Financial education plays a major role in successful money management. Unfortunately, many people never learn practical financial skills in school.

Reading books, listening to finance podcasts, following reliable financial experts, and learning basic investment principles can improve your confidence and decision-making.

The more you understand money, the easier it becomes to avoid scams, bad financial habits, and poor investment decisions.

Financial literacy also helps you recognize opportunities to grow wealth and improve your future.

You do not need to become a finance expert overnight. Even small improvements in knowledge can create major long-term benefits.

Set Financial Goals

Managing finances without goals can feel directionless. Goals provide motivation and help you stay focused during difficult periods.

Your financial goals may include:

- Paying off debt

- Buying a home

- Starting a business

- Saving for retirement

- Building passive income

- Traveling more

- Supporting your family

Break large goals into smaller steps so they feel achievable. Instead of saying you want to save a large amount of money someday, create a monthly savings target and timeline.

Tracking progress keeps you motivated and helps you stay accountable.

Control Emotional Spending

Emotions often influence spending decisions more than people realize. Stress, boredom, sadness, and social pressure can lead to impulsive purchases.

Online shopping and social media advertising make emotional spending even more common today.

Before buying something, take a moment to ask yourself whether the purchase is necessary or simply emotional.

A useful habit is waiting 24 hours before making non-essential purchases. This pause often reduces impulse buying and helps you make more thoughtful financial decisions.

Learning to control emotional spending can dramatically improve your financial health over time.

Plan for Retirement Early

Retirement may seem far away, especially for younger people, but starting early makes a huge difference.

The power of compound growth means money invested today can grow significantly over several decades.

Even small retirement contributions made consistently can become substantial over time.

Waiting too long to start saving for retirement usually means needing to contribute much larger amounts later.

The earlier you begin, the easier it becomes to build long-term financial security.

Review Your Finances Regularly

Managing finances is not a one-time task. Your income, expenses, goals, and responsibilities will change throughout life.

Review your financial situation regularly to make sure you are staying on track.

Check your budget, monitor savings progress, review debts, and adjust financial goals when needed.

Monthly financial reviews can help you catch problems early and improve decision-making before issues become serious.

Consistency is often more important than perfection.

F&Q

10 Innovative Tech & Software Tools That Make Work Easier

Technology has quietly become the gentle wind that moves modern work forward. Like a river…

10 Innovative Tech & Software Tools That Save Time and Money

Technology has quietly become part of almost every moment in our lives. From the first…

The Ultimate Digital Marketing Blueprint for Business Growth in 2026

The digital world moves like a flowing river. Every year, new platforms appear, customer expectations…

10 Powerful AI & Automation Tools That Save Time Every Day

This is where AI & Automation begins to make a meaningful difference. Instead of replacing…

10 Powerful Tools & Tutorials That Can Transform Your Daily Workflow

Every day brings a fresh opportunity to accomplish something meaningful, yet many of us find…

Best Tech & Software for Students, Professionals, and Creators

Technology has become one of the strongest driving forces behind education, business, and creativity. In…