Here is an even more conversational, down-to-earth version. It drops the remaining “article-style” structure and writes it exactly like a text from a close friend who has been there, done that, and genuinely wants to see you win.

Let’s be real for a second: managing money can feel like a total nightmare, especially when you’re just trying to figure it out. There’s this huge myth out there that financial planning is only for millionaires, tech CEOs, or Wall Street guys in suits.

Honestly? That’s total garbage. Financial planning is for literally everyone—whether you’re working a retail shift, freelancing from your couch, or trying to stretch your first entry-level paycheck.

At its core, it’s not about doing complex math or depriving yourself of everything fun. It’s just about knowing exactly where your money is going, figuring out what you want your life to look like in a few years, and making a game plan to get there. It gives you permission to make smart daily choices, dodge stressful debt, and actually sleep at night without that lingering cloud of financial anxiety.

The best part? You don’t have to fix everything today. If you take it one small step at a time, you can totally take control of your cash. Here is the realistic, no-BS guide to getting your money right.

Why You Actually Need a Plan

Without some sort of roadmap, your hard-earned money just sort of… evaporates. We’ve all been there: you look at your bank account on a Tuesday and wonder how on earth you spent $200 over the weekend. Plenty of people live paycheck to paycheck, not because they don’t make enough, but because they don’t have a strategy.

A good plan gives your money a job to do. It lets you buy the things you love right now while quietly setting you up for the big stuff later—like buying a house, traveling, or eventually retiring comfortably. Even the tiniest habits you start today will completely change your future.

Face Your Bank Account (Even If It Scares You)

Count the Incoming Cash: Total up everything you actually bring home—your main job, side gigs, selling stuff online, whatever.

Track the Bleeding: Be brutally honest about where it goes. Split it into the “must-pays” (rent, electric bill, groceries) and the “fun stuff” (dinners out, streaming services, late-night online shopping). Just tracking this for four weeks will blow your mind.

Do a Quick Inventory: What do you actually own (cash, savings) versus what do you owe (credit cards, student loans)? This is your baseline. No judgment, just data.

Set Goals That Get You Excited

- Saving money “just because” is boring, and it never works. You need actual destinations to keep you motivated. Give yourself something to look forward to:

Right Now (Short-term): Wiping out that annoying credit card or getting $1,000 into emergency savings.

Soon (Medium-term): Saving up for a reliable car, a vacation, or a security deposit on a better apartment.

Later (Long-term): Setting yourself up to buy a house or building financial independence so you can work on your own terms.

Pro-Tip: Stop saying, “I need to save money.” Start saying, “I’m going to save $2,500 for a trip by next summer.” Making it real makes it happen.

Build a Budget That Doesn’t Suck

- Budgeting gets a terrible reputation because people think it means eating ramen in the dark and never seeing your friends. But a real budget isn’t a cage—it’s a tool that gives you permission to spend without feeling guilty.

A great budget balances your bills, your future goals, and your current life. Use a simple rule of thumb: cover your absolute needs first, put a chunk toward your goals, and let yourself spend the rest on the things that actually make you happy. If you’re spending more than you make, don’t completely slash your social life—just make a few small trims. Consistency wins over perfection every single time.

Build a “Life Happens” Cushion

- Life loves to throw curveballs. Your car’s alternator dies, you drop your phone and shatter the screen, or you have an unexpected medical bill. An emergency fund is your ultimate safety net. It’s the difference between a minor inconvenience and a massive credit card crisis.

If money is tight, don’t stress about saving thousands right away. Putting away just $20 or $50 a paycheck adds up fast. Your ultimate goal is to get 3 to 6 months of basic living expenses sitting in a separate, high-yield savings account. Put it somewhere you won’t see it every day so you aren’t tempted to buy concert tickets with it.

Stop the Debt Snowball

- Debt is like dragging a giant anchor behind you while trying to run a marathon. High-interest debt (looking at you, credit cards) will absolutely eat your monthly cash flow alive if you let it.

Lay all your debts out on the table. Look at the balances and interest rates. Pick the one with the highest interest rate and attack it with everything you’ve got, while just paying the minimums on the rest. Once that first one is gone, move to the next. Watching those balances hit zero is one of the best feelings in the world.

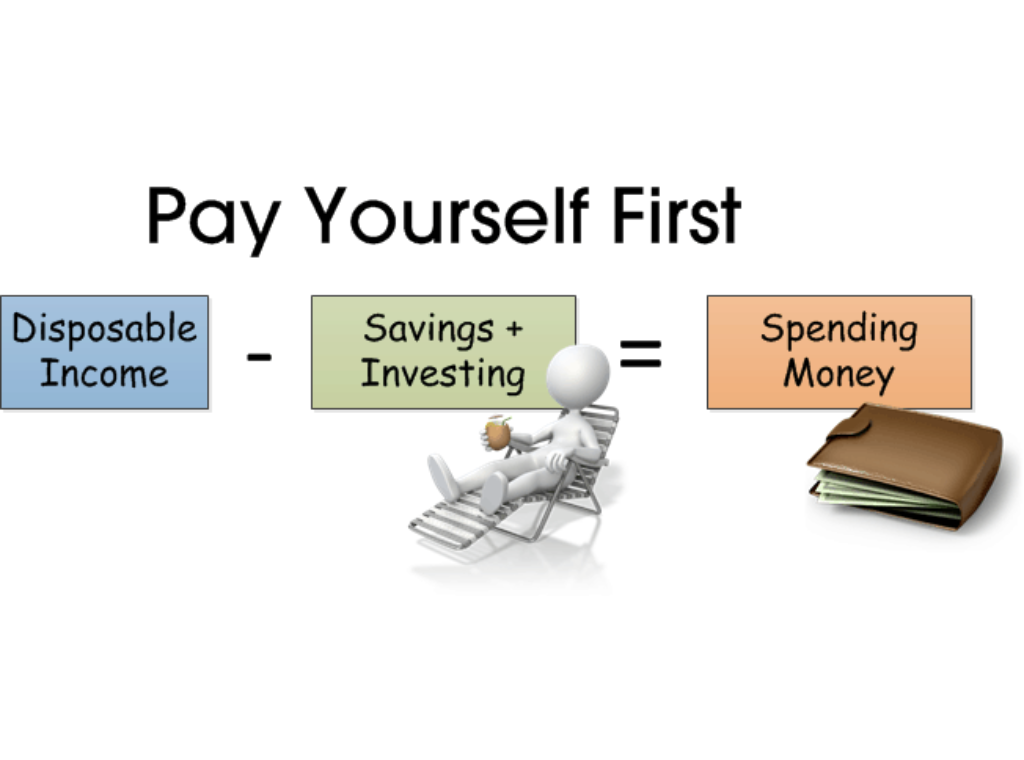

Pay Yourself First

- Most people pay their rent, pay for groceries, buy some clothes, go out for drinks, and then save whatever is “left over” at the end of the month. The problem? There is never anything left over.

Flip the script. Treat your savings like your absolute most important monthly bill. The easiest way to do this is to automate it. Set your bank account to automatically move $50 (or whatever you can afford) into your savings account the exact day your paycheck hits. If you never see it in your checking account, you won’t even miss it.

Make Investing Way Less Scary

- While savings accounts are great for short-term emergencies, inflation quietly eats away at your cash over time. If you want to actually build wealth, you have to let your money work for you while you sleep.

You do not need to be some stock-trading genius to do this. For beginners, the best move is to use low-cost index funds or jump on your employer’s retirement match plan if they offer one (that’s literally free money). The absolute secret weapon here is time. Because of compound interest, starting early with just $10 a week will beat starting late with $100 a week every single time.

Protect What You’re Building

You’re working incredibly hard to get your money right, so don’t let one bad accident ruin everything. A single uninsured emergency can completely wipe out years of progress.

Make sure you have basic guardrails in place:

Good health and auto insurance.

Renters or homeowners insurance (it’s way cheaper than you think).

A secure, organized digital folder where you keep photos of your ID, car title, and lease agreements so you aren’t scrambling if things go sideways.

Don’t Set It and Forget It

- Your life isn’t a script, and your financial plan shouldn’t be either. You’re going to change jobs, move to new places, get raises, or find new hobbies.

Put a reminder in your phone to check in on your money a few times a year. Give yourself a high-five for the goals you hit, and gently tweak your budget when life changes. Your plan needs to grow with you, not stress you out.

The Big Picture

You don’t need an Ivy League degree or a six-figure salary to be good with money. True financial success isn’t about hitting the lottery or making one perfect decision. It’s just the result of a bunch of small, quiet, daily choices that align with what makes you happy.

The hardest part is literally just starting. Pick one thing from this list to do this week—whether that’s opening a savings account or tracking your coffee spending—and just do that. You’ve got this!

FAQ’s

1. What is financial planning?

Financial planning is the process of managing money to achieve short-term and long-term goals.

2. Why is financial planning important?

It helps control spending, reduce debt, build savings, and secure your future.

3. How much should I save for emergencies?

Aim for 3–6 months of essential living expenses.

4. When should beginners start investing?

As early as possible, after building an emergency fund and managing high-interest debt.

5. How often should I review my financial plan?

At least once every six months or whenever major life changes occur.

10 Innovative Tech & Software Tools That Make Work Easier

Technology has quietly become the gentle wind that moves modern work forward. Like a river…

10 Innovative Tech & Software Tools That Save Time and Money

Technology has quietly become part of almost every moment in our lives. From the first…

The Ultimate Digital Marketing Blueprint for Business Growth in 2026

The digital world moves like a flowing river. Every year, new platforms appear, customer expectations…

10 Powerful AI & Automation Tools That Save Time Every Day

This is where AI & Automation begins to make a meaningful difference. Instead of replacing…

10 Powerful Tools & Tutorials That Can Transform Your Daily Workflow

Every day brings a fresh opportunity to accomplish something meaningful, yet many of us find…

Best Tech & Software for Students, Professionals, and Creators

Technology has become one of the strongest driving forces behind education, business, and creativity. In…