Financial stability is something many people want, but not everyone understands how to achieve it. Some believe financial stability only means becoming rich, while others think it requires a very high salary. In reality, financial stability is less about how much money you earn and more about how well you manage the money you have.

Being financially stable means having control over your finances, being able to cover your expenses comfortably, and preparing for future needs without constant stress. It gives you peace of mind and the freedom to make better decisions in life. Financial stability does not happen overnight. It is built gradually through smart habits, patience, and discipline.

No matter your current income level, it is possible to improve your financial situation step by step. The key is understanding where your money goes, making thoughtful decisions, and creating long-term financial habits that support stability.

Understand Your Current Financial Situation

The first step toward financial stability is understanding your current financial condition honestly. Many people avoid looking closely at their finances because it feels stressful or overwhelming. However, ignoring financial problems only makes them harder to solve.

Start by calculating your monthly income and expenses. Write down everything you spend money on, including rent, food, transportation, subscriptions, entertainment, and small daily purchases. This gives you a clear picture of your financial habits.

Once you see where your money is going, it becomes easier to identify areas where you can reduce unnecessary spending. Financial awareness is the foundation of financial stability because you cannot improve what you do not understand.

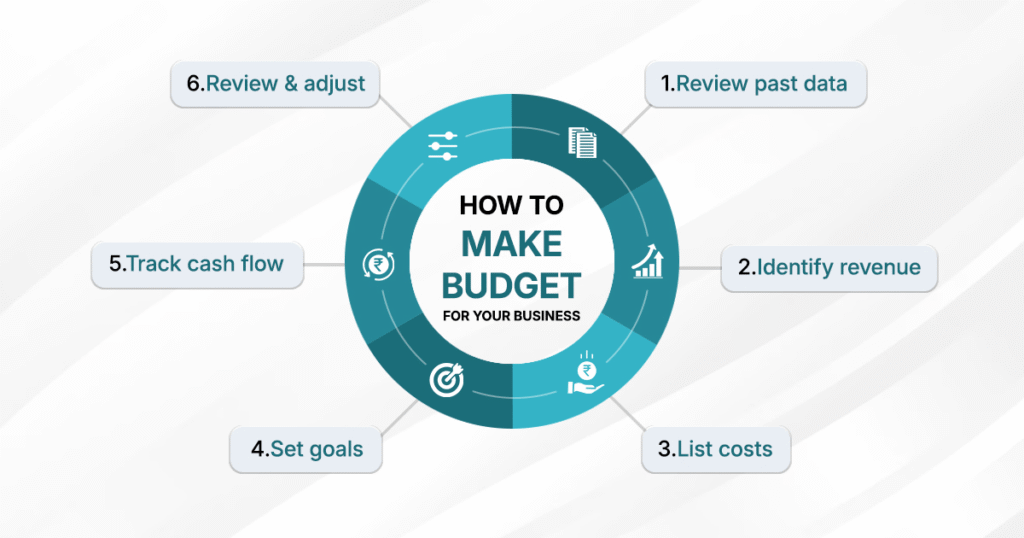

Create a Realistic Budget

A budget is one of the most important tools for managing money effectively. Many people think budgeting means restricting yourself completely, but a good budget actually gives you more control and freedom.

The purpose of a budget is to ensure your spending matches your financial goals. Divide your income into categories such as necessities, savings, investments, debt payments, and personal spending.

The key is creating a realistic budget that you can actually follow. Extremely strict budgets often fail because they become difficult to maintain long term. Instead, focus on balance and consistency.

Review your budget regularly and adjust it when needed. Life circumstances change, and your financial plan should adapt accordingly.

Build an Emergency Fund

Unexpected expenses are one of the biggest reasons people struggle financially. Medical bills, job loss, car repairs, or family emergencies can quickly create financial stress if you are unprepared.

An emergency fund acts as a financial safety net. It helps you handle unexpected situations without relying on loans or credit cards.

Start small if necessary. Even saving a little each month builds momentum over time. Ideally, an emergency fund should cover at least three to six months of essential living expenses.

Having emergency savings not only improves financial security but also reduces anxiety and stress about the future.

Reduce Unnecessary Debt

Debt can make financial stability difficult, especially when high-interest payments consume a large portion of your income. While some forms of debt may be manageable, uncontrolled debt creates long-term financial pressure.

Start by identifying all your debts, including credit cards, loans, and other obligations. Focus on paying off high-interest debt first because it grows the fastest.

Avoid taking on new debt unless absolutely necessary. Many people fall into financial problems because they use credit for unnecessary purchases instead of living within their means.

Reducing debt improves cash flow, lowers stress, and allows you to focus more on saving and investing.

Develop Better Spending Habits

Financial stability depends heavily on daily habits. Small spending decisions repeated consistently can either improve or damage your financial health.

Impulse buying is one of the biggest obstacles to saving money. Before making non-essential purchases, take time to ask yourself whether the item is truly necessary.

Another helpful habit is comparing prices before buying something. Small savings on regular purchases can add up significantly over time.

Learning to separate wants from needs is essential. This does not mean you should never enjoy your money, but it means making thoughtful choices instead of emotional spending decisions.

Increase Your Income Over Time

While managing expenses is important, increasing your income also plays a major role in achieving financial stability.

Improving your skills, gaining experience, or learning new abilities can help you qualify for better job opportunities and higher income. Investing in education or skill development often creates long-term financial benefits.

Some people also explore side income opportunities such as freelancing, online businesses, part-time work, or investments. Multiple income sources provide greater financial security because you are not completely dependent on one source.

However, increasing income alone will not solve financial problems if spending habits remain unhealthy. Financial stability requires both earning wisely and managing money responsibly.

Start Saving Consistently

Saving money is one of the most important financial habits. Many people wait until they have extra money to save, but financial stability usually comes from saving consistently regardless of income level.

Treat savings like a regular monthly expense rather than something optional. Even small amounts saved regularly can grow significantly over time.

Automating savings can make the process easier. Setting up automatic transfers to a savings account reduces the temptation to spend the money elsewhere.

Consistency matters more than the amount initially. Building the habit of saving creates long-term financial discipline.

Learn Basic Investing

Saving money alone may not always be enough for long-term financial growth because inflation gradually reduces the value of money over time. Learning basic investing can help your money grow more effectively.

Investing does not have to be complicated. Understanding simple concepts such as mutual funds, stocks, retirement accounts, or fixed investments can help you make better financial decisions.

The goal of investing is long-term growth, not quick profits. Many financially stable people build wealth slowly through consistent and patient investing strategies.

It is important to learn before investing and avoid making emotional decisions based on fear or excitement.

Avoid Lifestyle Inflation

One common financial mistake is increasing spending every time income increases. This is known as lifestyle inflation.

When people earn more money, they often upgrade their lifestyle immediately by buying expensive items, larger homes, or luxury products. While enjoying success is fine, uncontrolled lifestyle inflation can prevent long-term financial stability.

Instead of increasing expenses dramatically, use additional income to improve savings, investments, and financial security.

Financial stability is often built by maintaining balance even as income grows.

Focus on Long-Term Financial Goals

Financial stability becomes easier when you have clear goals. Goals provide direction and motivation for your financial decisions.

Examples of long-term goals include buying a home, retiring comfortably, starting a business, traveling, or becoming debt-free.

Breaking large goals into smaller steps makes them feel more achievable. Progress may feel slow at times, but consistent effort creates meaningful results over the years.

Long-term thinking also helps reduce impulsive financial decisions because you become more focused on future benefits rather than short-term satisfaction.

Improve Financial Knowledge

Financial education is one of the most valuable investments you can make in yourself. Unfortunately, many people are never taught practical money management skills.

Reading books, listening to financial experts, and learning about budgeting, saving, taxes, and investing can significantly improve your financial confidence.

The more you understand money, the better decisions you will make. Financial knowledge reduces fear and gives you more control over your future.

Practice Patience and Discipline

Financial stability is not built quickly. Many people become discouraged because they expect immediate results. However, real financial progress usually happens gradually.

Patience is important because financial habits take time to show results. Discipline is important because consistency matters more than motivation.

There will be setbacks and unexpected challenges along the way, but staying committed to your financial goals makes a huge difference over time.

F&Q

10 Innovative Tech & Software Tools That Make Work Easier

Technology has quietly become the gentle wind that moves modern work forward. Like a river…

10 Innovative Tech & Software Tools That Save Time and Money

Technology has quietly become part of almost every moment in our lives. From the first…

The Ultimate Digital Marketing Blueprint for Business Growth in 2026

The digital world moves like a flowing river. Every year, new platforms appear, customer expectations…

10 Powerful AI & Automation Tools That Save Time Every Day

This is where AI & Automation begins to make a meaningful difference. Instead of replacing…

10 Powerful Tools & Tutorials That Can Transform Your Daily Workflow

Every day brings a fresh opportunity to accomplish something meaningful, yet many of us find…

Best Tech & Software for Students, Professionals, and Creators

Technology has become one of the strongest driving forces behind education, business, and creativity. In…